EL PROYECTO

OTRAS ESTRATEGIAS NEUTRALES

- Iron Condor

- Short Straddle

- Short Strangle

- Butterfly Spread

- Calendar Spread

- Ratio Spread

¿De qué trata este sitio web?

Este proyecto nace después de un extenso período de exploración e investigación en busca de diversas formas de obtener ganancias en el mundo del mercado financiero. Debo admitir que encontré muchas estrategias, pero no todas resultaron ser rentables a largo plazo.

Numerosas estrategias se basan en indicadores, osciladores o la acción del precio, sin embargo, no conseguí identificar una que me permitiera evaluar a largo plazo la probabilidad y eficacia de una estrategia.

Por esta razón, comencé a buscar estrategias fundamentadas en patrones, desechando completamente el análisis técnico y fundamental, y centrándome exclusivamente en el comportamiento del mercado durante ciertos intervalos de tiempo.

Sabemos que en el mundo de las opciones existen estrategias alcistas, bajistas y neutrales. Y también sabemos, respaldados por estadísticas a largo plazo, que el mercado tiende a moverse en su mayoría de manera lateral.

A pesar de los momentos alcistas y bajistas ocasionales, la mayor parte del tiempo el mercado se caracteriza por su movimiento lateral. Incluso este fenómeno puede extrapolarse al intradía, donde dentro de un mismo día, existe un período horario en el cual el mercado tiende a estabilizarse y a comportarse de manera lateral. ¿Cuándo ocurre esto? Sucede cuando la naturaleza humana busca descanso y alimentación. Digamos que entre las 11:00am y la 1:00pm. Sin embargo tambien es aplicable a otros rangos horarios.

Pues bien, partiendo de estas premisas (lateralidad y rango de tiempo) empece por buscar una estrategia neutral en el mundo de las opciones finacieras. Una de las mas conocidas es la denominada Iron Butterfly.

¿De qué trata la estrategia?

Basada en las ciencias de las matemáticas y las estadísticas, una estrategia se conforma por cientos de operaciones repetitvas bajo los mismos parametros y circunstancias predefinidas que llevaran a obtener una esperanza matemática a largo plazo. Si esa esperanza matematica es positva, la estrategia sera ganadora, de lo contrario sera perdedora. En pocas palabras: repetir, repetir, repetir.

En resumen, la repetición constante de estas operaciones según la estrategia establecida se convierte en el núcleo de su éxito, destacando la importancia de la constancia y la disciplina en la implementación de dicho enfoque. Este enfoque repetitivo y estructurado es esencial para alcanzar los objetivos deseados y minimizar la influencia de las fluctuaciones a corto plazo.

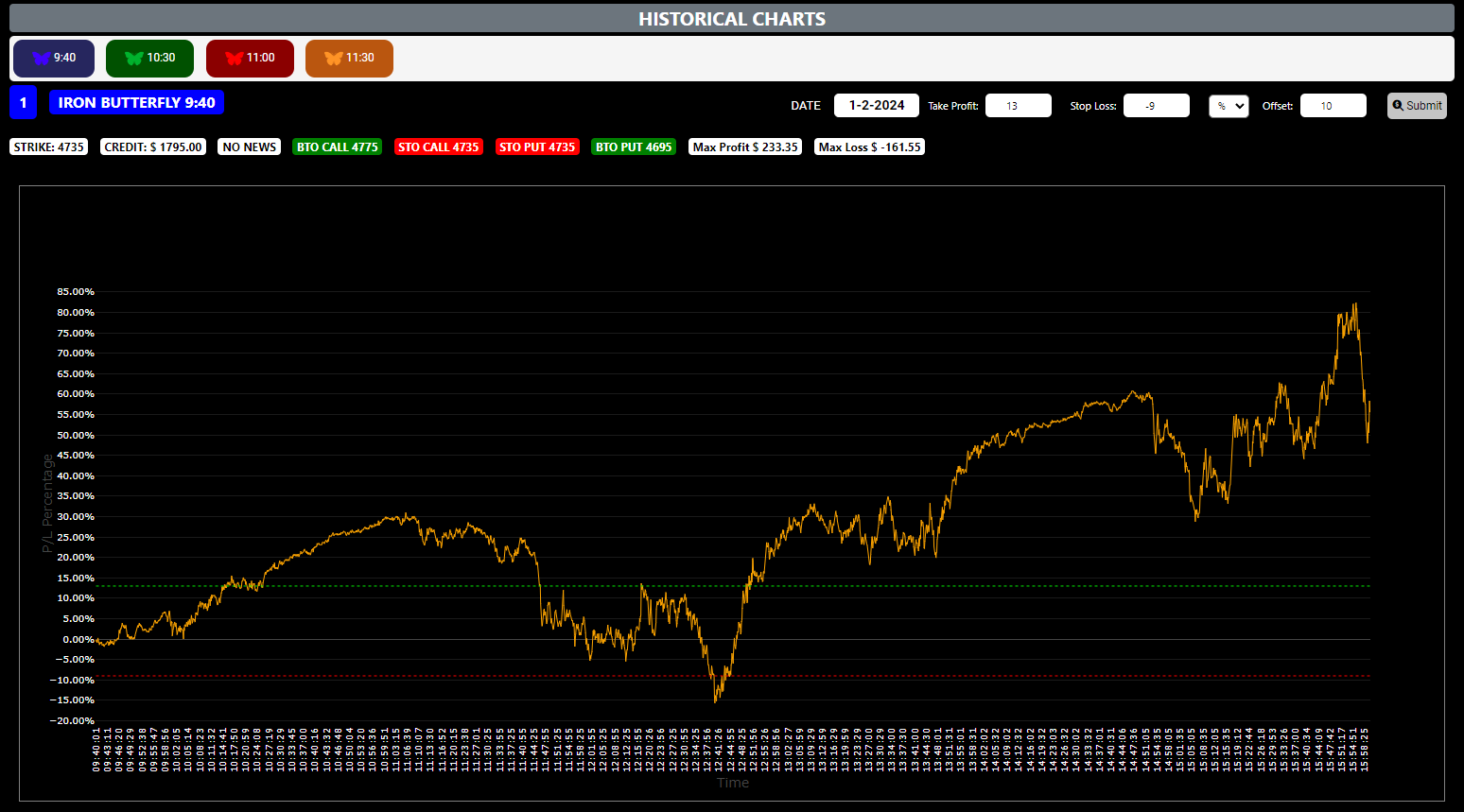

BACKTESTING

Los datos se recopilan diariamente y a partir del horario correspondiente a cada estrategia. El intervalo es cada 6 O 7 segundos aproximadamente. Cada entrada se conforma de:

| ESTRATEGIA # | TIMESTAMP | PRICE | SPX LAST |

| IB 9:40 | 09:40:05 | 1850.50 | 4735.25 |

| IB 9:40 | 09:40:11 | 1845.00 | 4736.20 |

| IB 9:40 | 09:40:17 | 1840.30 | 4736.25 |

| IB 9:40 | 09:40:24 | 1847.50 | 4736.65 |

Con estos datos obtenidos durante la sesion, podremos obtener una linea grafica del comportamiento del iron butterfly para la estrategia horaria seleccionada.

Conformacion de la estrategia

- Definir previamente los días donde haya noticias importantes y esto afecte a la volatilidad del mercado. (Ej: días con reportes de desempleo, inflación, reuniones de FOMC, etc).

- Elegir un horario y abrir un Iron Butterfly con los mismos anchos de alas.

- Definir el Take Profit y Stop Loss correspondiente.

PARAMETROS

1. Eleccion de la estrategia

Dentro del mundo de las opciones existen muchas estrategias. Alcistas, bajistas y neutrales. Dado que el mercado tiende a mantenerse mas tiempo en posicion lateral, se escogió una que abarcara el sesgo neutral. Y dentro de la lista de estragegias neutrales, se escogió el Iron Butterfly.

2. Eleccion del subyacente

A la hora de definir el subyacente al cual dirigir la estrategia, se buscó un indice en lugar de una accion, futuro o ETF. Debia tener buena liquidez y volumen por lo que se escogio el Standard & Poor 500.

3. DIAS VOLATILES

Despues de un backtesting de mas de un año, se detectaron que hay 4 o 5 eventos o reportes que hacen mover con mas fuerza la volatilidad de los mercados diariamente. Estos dias NO se abrira ninguna operacion:

4. HORARIO

Si bien la principal estrategia de Iron Butterfly que se testeó fue la de aperturar a las 11:30am (ya que era un horario donde la volatilidad y movimientos empiezan a decrecer), se decidió empezar a hacer backtesting de otros 3 horarios: 9:40am, 10:30am y 11:00am. Esto favoreció el hecho de que se pudieran obtener patrones, movimientos y escenarios diferentes que luego al compararlos generarian interesantes resultados.

En cuanto al ancho de las alas, arbitrariamente se decidio utilizar una distancia de 40 puntos. Mas adelante, y siguiendo la linea del projecto, seria interesante agregar otros anchos de alas, otros horarios, incluso con otras condiciones de apertura.